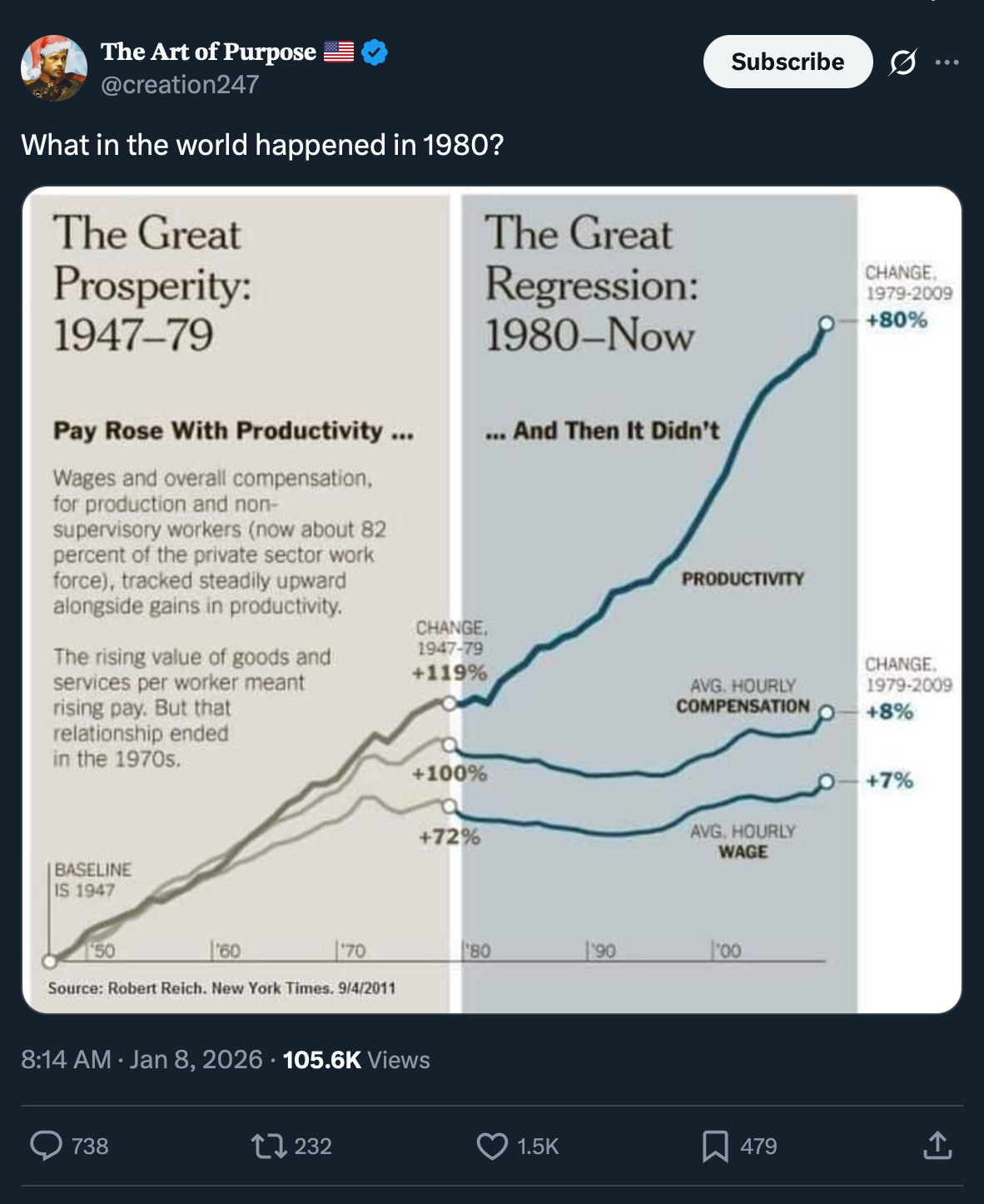

I was looking at a chart recently that you have probably seen floating around financial Twitter or LinkedIn. It tracks two lines: productivity and compensation.

From 1948 until the early 1970s, these two lines moved in perfect lockstep. If workers produced more value, they got paid more money. It was a simple, logical correlation.

But starting around 1971, the lines split. Productivity continued to skyrocket—up over 250% since 1948—while compensation flatlined. This is often called “The Great Decoupling.”

I wanted to understand the mechanics behind this. It isn’t just corporate greed or political policy; it is largely a function of monetary physics. I dug into the history of the US dollar, the removal of the gold standard, and a concept known as the Cantillon Effect to find out why working harder no longer guarantees you make more money.

Here is what I found.

Nixon Shock: August 15, 1971

To understand why your paycheck feels smaller despite you doing more work, we have to look at the Nixon Shock.

From the 1950s through the 1960s, the US operated on the gold standard. Every ounce of gold was pegged at $35. Foreign countries could essentially walk up to the US Treasury, hand over dollars, and request physical gold bars in return. This kept spending in check because money was tied to a physical constraint.

But in the late 60s, the US was spending heavily. Foreign nations began to doubt the US had enough gold to back its dollars. They started trading in their paper money for metal. Fearing a “run on the bank,” President Richard Nixon suspended the convertibility of the dollar into gold.

The dollar became a fiat currency. It was no longer backed by a commodity but by the “full faith and credit” of the government. This severed the anchor between productivity and money creation.

The Cantillon Effect: It Matters Who Gets the Money First

This is where Richard Cantillon enters the picture. He was an 18th-century economist who theorized that money is not neutral. He argued that where money enters the economy matters just as much as how much enters.

He used the analogy of pouring honey into a saucer.

- The honey piles up in the center first (the injection point).

- It takes a long time to slowly spread out to the rim.

In our modern economy, the central bank pours the “honey.” But they don’t pour it into everyone’s bank accounts equally. They pour it into the financial sector.

The Flow of Money

- Early Receivers (The Center): The government, commercial banks, and large investors get the new money first via bonds and loans.

- Late Receivers (The Rim): Wage earners, pensioners, and hourly workers get the money last.

Purchasing Power Arbitrage

The problem with being a late receiver is inflation.

When the “Early Receivers” get the new money, prices in the economy haven’t risen yet. They get to use this cheap capital to buy assets—stocks, real estate, and companies—at yesterday’s prices. This drives up the value of those assets.

By the time that money trickles down to the “Late Receivers” in the form of wages, the new money has already circulated through the system. The price of housing, food, and gas has already gone up.

I looked at the data on the M2 Money Supply to visualize this:

- 1971: ~$710 Billion in circulation.

- Today: ~$22.3 Trillion in circulation.

That is a 31x explosion in the money supply. This massive injection of liquidity flowed primarily into financial assets rather than wages. This creates a wealth transfer. The value created by increased productivity wasn’t shared as wages; it was siphoned off into asset inflation.

The AI Question

We talk a lot about AI and productivity tools here. The promise is that AI will make us all exponentially more productive.

But if we look at the chart from 1971 to today, we have to ask a difficult question: If AI doubles our productivity again, who keeps the profit?

Based on the Cantillon Effect, the benefits of this productivity boom will likely accrue to the people who own the assets—the servers, the models, and the company equity—rather than the people doing the work. If you are selling your time for a wage, you are standing at the back of the line.

Key Takeaways

- The Decoupling: Wages stopped tracking with productivity in 1971 when the US moved to a fiat currency system.

- Money Entry Points: New money enters the economy through banks and investors first, giving them a purchasing power advantage.

- The Inflation Tax: Wage earners are “late receivers.” By the time new money reaches your paycheck, the cost of living has already risen.

- Asset vs. Wage: The current system rewards asset ownership over labor.

Want to earn CPE for this topic?

- Compare Options: See how we stack up against others in our 2025 Flexible CPE Guide

- Understand the Format: Read how Nano-Learning works for CPAs.

- Check Your State: Ensure you are compliant with our State Requirements Guide.

- What is EverydayCPE?

Related Courses:

{kind=link}